The Global Mobility Property Cycle: Why Countries First Invite Expats — Then Push Them Out

The Global Mobility Property Cycle: Why Countries First Invite Expats — Then Push Them Out

Portugal welcomed digital nomads.

The Netherlands competed aggressively for international talent.

Spain benefited from foreign demand and tourism-driven investment.

Dubai built entire ecosystems around globally mobile capital.

Then rents surged.

Housing shortages intensified.

Political pressure followed.

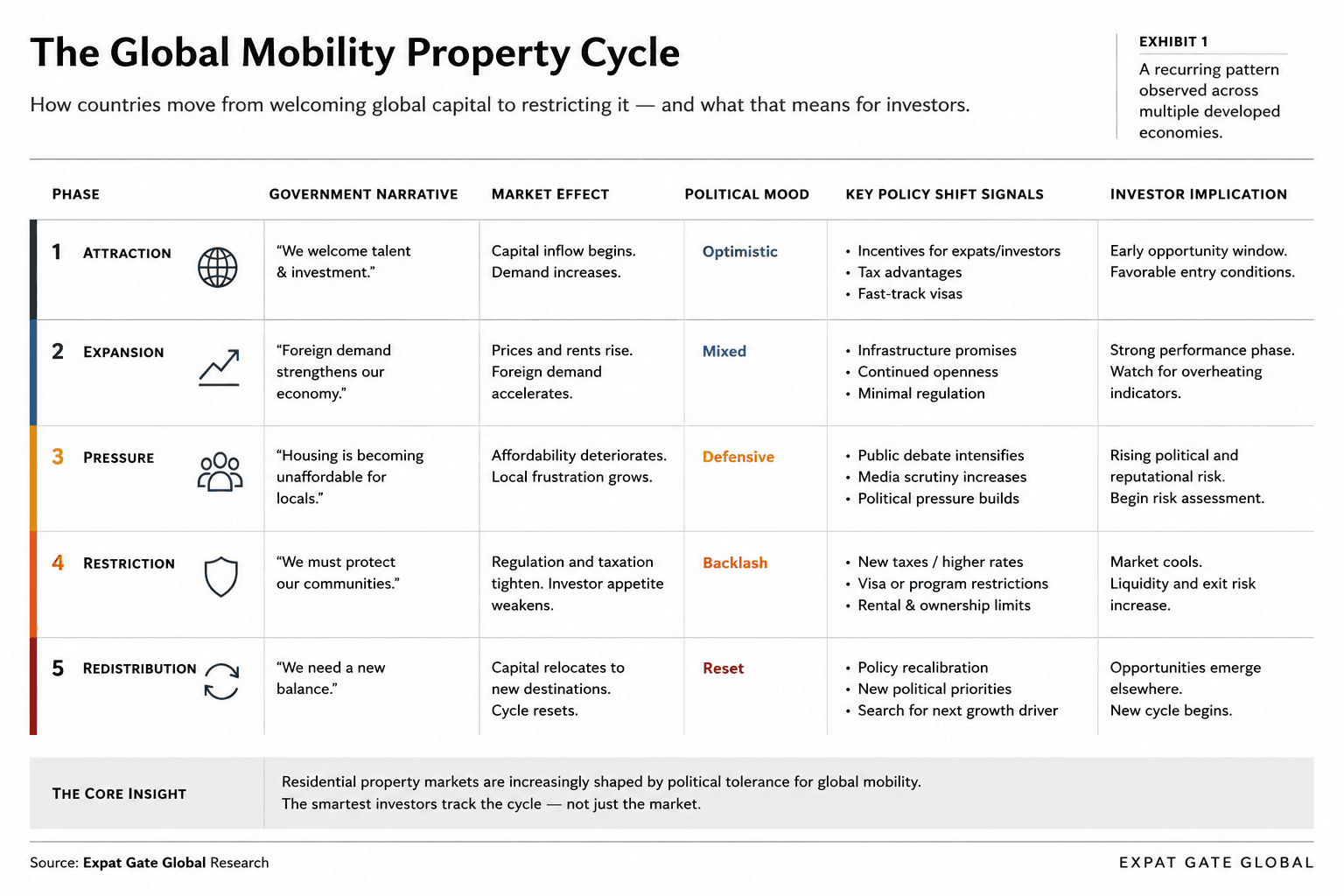

Increasingly, countries appear to be moving through the same cycle: attract foreign capital, stimulate demand, experience housing stress, tighten regulation, and eventually push part of that capital elsewhere.

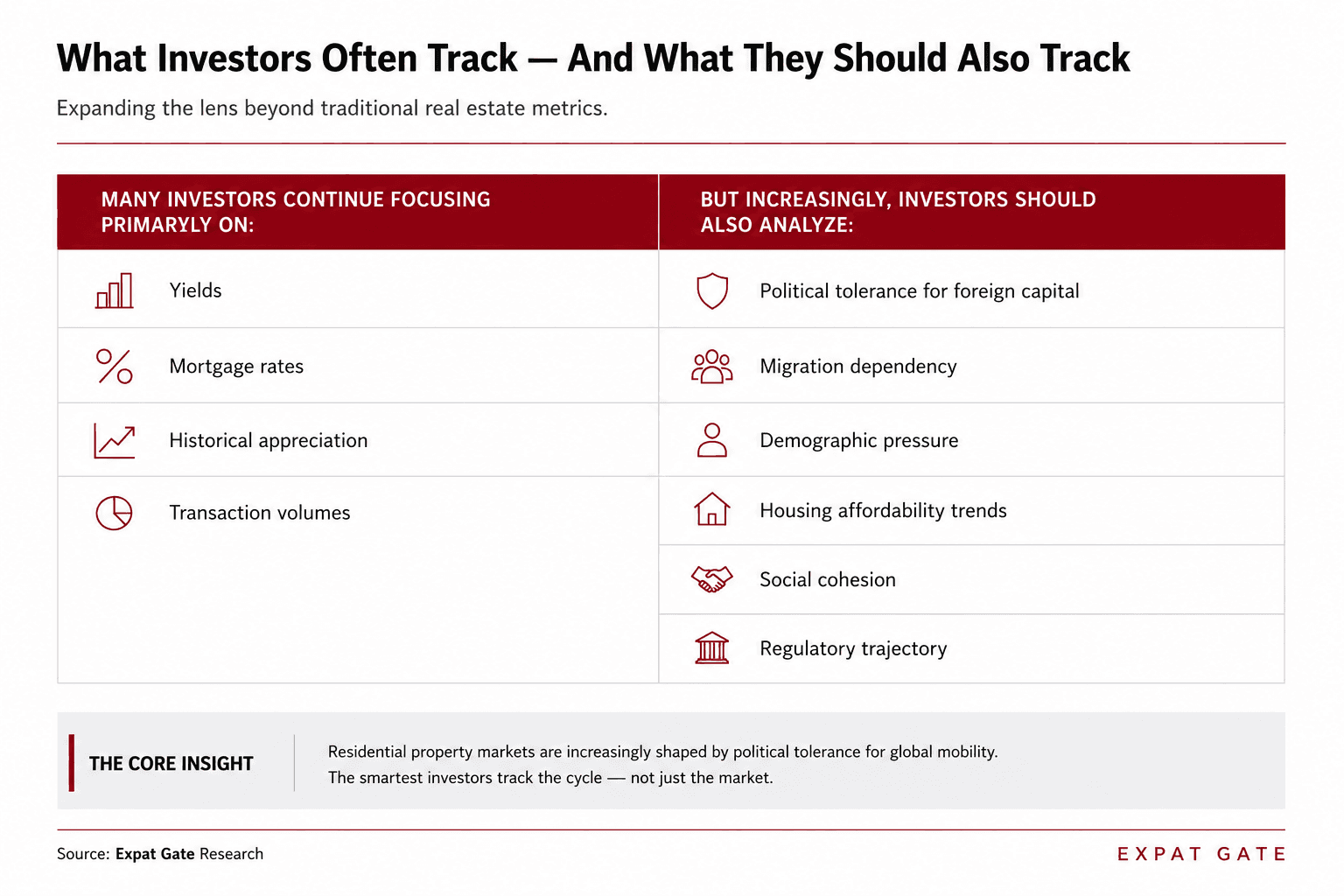

For years, residential property investors mostly focused on traditional indicators:

mortgage rates;

price-per-square-meter trends;

supply levels;

historical appreciation.

Those factors still matter. But they no longer explain the full picture.

Residential real estate is becoming increasingly shaped by something larger: global mobility flows — and the political tolerance for them.

Expat Gate Thesis

The global competition for internationally mobile people and capital has intensified dramatically over the past decade.

Countries increasingly compete to attract:

highly skilled migrants;

founders;

remote workers;

digital nomads;

affluent international families;

and globally mobile investors.

At first, the effects are usually positive:

more spending;

more investment;

stronger local economies;

rising property values;

international visibility.

But successful inflows often create a second phase:

housing pressure.

And once housing affordability deteriorates enough, the political narrative begins to change.

What started as:

“We welcome global talent”

can gradually evolve into:

“Housing is becoming unaffordable for locals.”

That shift matters enormously for property investors.

Because increasingly, residential markets are influenced not only by economics — but also by social tolerance for foreign capital and migration.

Not every country moves through this cycle at the same speed.

Some may remain structurally attractive for decades.

Others may reverse course politically.

But the broader pattern is becoming increasingly visible across multiple regions.

Portugal: From Expat Darling to Political Pressure

Portugal became one of the most visible examples of the “open phase” of the cycle.

The country successfully attracted:

remote workers;

retirees;

entrepreneurs;

foreign property buyers;

and internationally mobile professionals.

Programs such as the Non-Habitual Resident (NHR) tax regime and Golden Visa helped fuel international demand.

For years, Portugal was presented globally as a model destination:

safe, affordable, sunny, European, and internationally accessible.

That strategy worked.

But success created pressure.

Housing affordability became a growing political issue, especially in Lisbon and Porto. Public debate around foreign buyers, short-term rentals, and expat-driven price growth intensified.

Eventually, political momentum shifted:

Golden Visa rules were tightened;

housing regulation became more interventionist;

the tone of the debate changed significantly.

The important signal was not any single regulation.

The signal was the transition in political mood.

The Netherlands: Talent Attraction Meets Housing Constraints

The Netherlands followed a different version of the same dynamic.

For years, the country actively positioned itself as a hub for:

international business;

tech talent;

multinational headquarters;

and highly skilled migrants.

Amsterdam especially benefited from this strategy.

At the same time, the country faced:

limited housing supply;

increasing population pressure;

rising rents;

and growing affordability concerns.

Over time, housing became one of the most politically sensitive issues in Dutch society.

The response increasingly included:

stricter rental regulation;

pressure on landlords;

taxation changes;

and broader political scrutiny around the housing market itself.

Again, the key observation is not whether specific policies were “right” or “wrong.”

The more important point is that housing markets increasingly evolve within broader social and political cycles — not purely economic ones.

Spain: Tourism, Foreign Demand and Backlash

Spain presents another variation.

In several Spanish cities and coastal regions, tourism and foreign demand became deeply intertwined with local housing markets.

In some areas, this contributed to:

rapid rent growth;

short-term rental expansion;

and affordability pressure for residents.

Public protests around tourism and housing intensified in multiple regions.

Once again, the most important signal was not a single protest or headline.

It was the broader shift in public sentiment:

the growing perception that parts of the housing market were increasingly serving external demand more than local residents.

That perception alone can eventually reshape regulation, taxation, and political priorities.

Canada: A Clear Regulatory Signal

Canada offers one of the clearest examples of direct government intervention.

Concerns around affordability and foreign demand contributed to:

foreign buyer restrictions;

vacancy taxes;

and broader debates around housing accessibility.

Regardless of one’s political view, the strategic implication for investors is significant:

residential property is becoming increasingly exposed to political reaction risk.

That was far less true twenty years ago than it is today.

Hidden Signal

The next major real estate trend may not emerge from property data first.

It may emerge from:

migration debates;

tax policy;

political rhetoric;

school capacity pressure;

healthcare strain;

anti-tourism sentiment;

or discussions around “who cities are being built for.”

Many investors still analyze residential property as a largely local asset class.

Increasingly, that assumption looks incomplete.

Residential markets are becoming more interconnected with:

global mobility;

remote work;

geopolitics;

tax competition;

lifestyle migration;

and internationally mobile capital.

The most important signals may therefore appear outside traditional real estate news entirely.

What Could Go Wrong With This Thesis

This framework is not universal.

Some countries may remain strongly pro-capital and pro-migration for decades.

Others may successfully expand housing supply and reduce pressure before political backlash intensifies.

In certain cases, demographic decline may even force governments to remain highly dependent on international inflows.

The cycle is therefore not deterministic.

But the broader pattern is becoming increasingly difficult to ignore.

Bottom Line

Residential property is no longer shaped only by local economics.

It is increasingly shaped by global mobility flows — and by how societies react to them.

The future of residential real estate may depend less on square meters alone, and more on political tolerance for globally mobile capital.

And increasingly, the next major market shift may begin outside real estate itself.